Welcome to an exhilarating journey into the world of regression! In this edition of Stat Quest, we will delve into the captivating realm of Lasso Regression, a close cousin of Ridge Regression. Prepare to be amazed as we unravel the mysteries of Lasso Regression and discover its remarkable distinctions.

The Similarities and the Differences

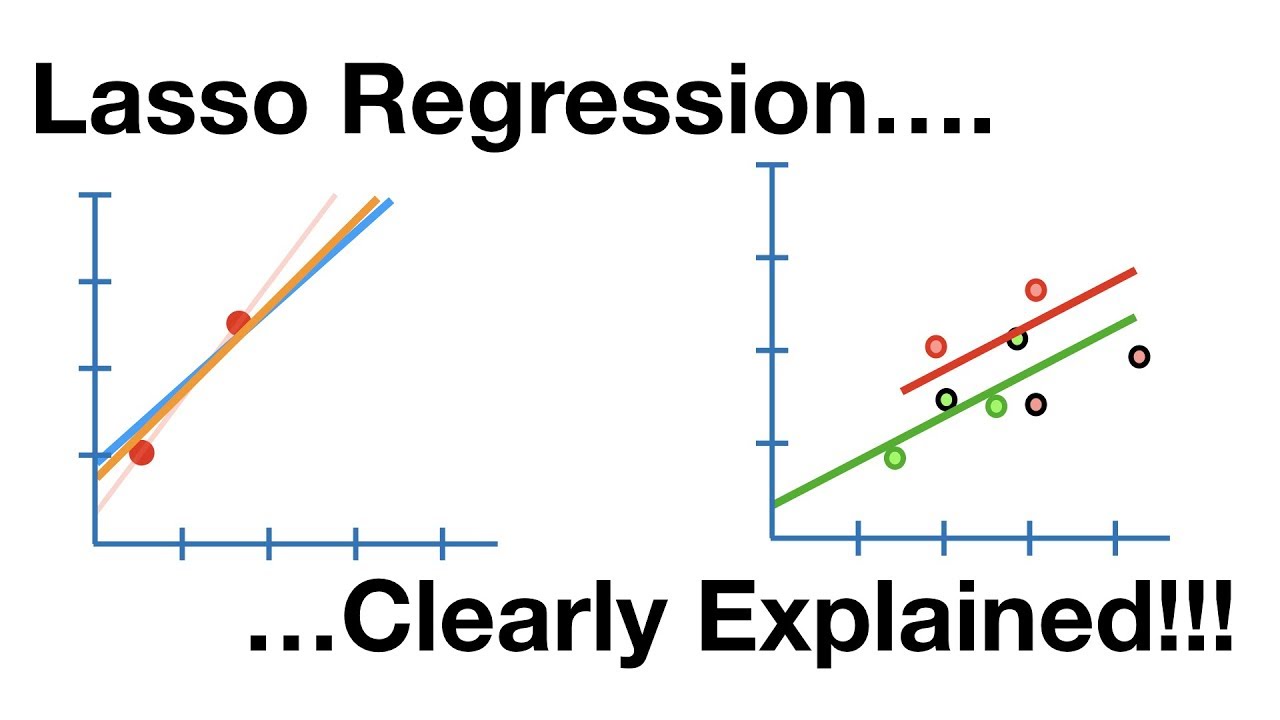

Before we immerse ourselves in the enchanting world of Lasso Regression, let’s do a quick recap of Ridge Regression. In a previous Stat Quest, we explored weight and size measurements of mice, dividing the data into training and testing sets. Utilizing the power of least squares, we fit a line to the training data, minimizing the sum of squared residuals. However, this seemingly perfect fit had its drawbacks when it came to testing data. It lacked the ability to generalize well, leading to a high variance.

Enter Ridge Regression. By adding a penalty term, lambda times the slope squared, we achieved a more balanced solution. The resulting Ridge Regression line exhibited a slight increase in bias but a significant reduction in variance. The secret lay in sacrificing a bit of bias for the sake of long-term predictions. This is where Lasso Regression enters the scene.

The Lasso Regression Penality

In Lasso Regression, instead of squaring the slope like in Ridge Regression, we take the absolute value. Similar to Ridge Regression, lambda can take any value from 0 to positive infinity and is determined through cross-validation. The Lasso Regression line, denoted by an elegant shade of orange, exhibits a tad more bias than least squares but significantly less variance. The magic lies in its ability to make predictions less sensitive to tiny training datasets.

Both Ridge and Lasso Regression can be applied to various scenarios. For example, in predicting size based on two different diets or using weight to predict obesity. They can even be employed in complex models that combine different data types. Intriguingly, the Lasso Regression penalty excludes all estimated parameters, except for the y-intercept. This contrasts with its Ridge counterpart, where all parameters are included.

As we increase the value of lambda in Lasso Regression, the slope gradually diminishes. Astonishingly, it can shrink all the way to zero, unlike Ridge Regression, which can only asymptotically approach zero. By excluding useless variables from equations, Lasso Regression triumphs in simplifying the final equation and making it more interpretable.

Embracing the Differences

In summary, while Ridge and Lasso Regression may seem similar at first glance, they possess distinctive characteristics. Ridge Regression squares the variables, whereas Lasso Regression takes the absolute value. However, the real distinction lies in Lasso Regression’s ability to exclude useless variables, transforming complex equations into elegant and insightful predictions. Ridge Regression, on the other hand, thrives when most variables are useful.

Congratulations! You have successfully reached the end of this thrilling Stat Quest adventure. If you relished this journey and thirst for more, be sure to subscribe. And if you want to support Stat Quest further, consider indulging in one or two original songs. Until our paths cross again, quest on!